We will start by picking up some data from Yahoo Finance APIs

Código

import yfinance as yf#getting historic stock data from yfinancestocks_list = ['BBDC4.SA', 'ITUB4.SA','SANB4.SA', 'BBAS3.SA']data = yf.download(stocks_list, period='5y')['Close']data

Ticker

BBAS3.SA

BBDC4.SA

ITUB4.SA

SANB4.SA

Date

2020-11-23

11.589112

14.348302

20.156155

14.215531

2020-11-24

11.897979

14.993038

20.721098

14.784431

2020-11-25

11.864407

14.799619

20.476992

15.099722

2020-11-26

11.676399

14.559301

20.044575

15.264223

2020-11-27

11.619331

14.442083

20.198011

15.181969

...

...

...

...

...

2025-11-14

22.440001

19.469999

40.599998

17.500000

2025-11-17

22.500000

19.320000

40.299999

17.270000

2025-11-18

21.879999

19.090000

40.099998

17.330000

2025-11-19

21.580000

18.900000

39.849998

17.129999

2025-11-21

22.000000

18.790001

39.970001

17.150000

1247 rows × 4 columns

Then we transform data to build log returns:

Código

# function to build log returns from a dataframedef log_returns(df):import numpy as np df_ = df.copy()for stock in df.columns: df_[stock] = np.log(df_[stock]).diff()return df_.dropna()

Código

# applying the functiondaily_returns = log_returns(data)daily_returns

Ticker

BBAS3.SA

BBDC4.SA

ITUB4.SA

SANB4.SA

Date

2020-11-24

0.026302

0.043954

0.027643

0.039240

2020-11-25

-0.002826

-0.012985

-0.011851

0.021102

2020-11-26

-0.015973

-0.016371

-0.021343

0.010835

2020-11-27

-0.004899

-0.008084

0.007626

-0.005403

2020-11-30

-0.021908

-0.013895

-0.013909

-0.050462

...

...

...

...

...

2025-11-14

-0.002670

-0.000513

0.003949

0.014969

2025-11-17

0.002670

-0.007734

-0.007417

-0.013230

2025-11-18

-0.027942

-0.011976

-0.004975

0.003468

2025-11-19

-0.013806

-0.010003

-0.006254

-0.011608

2025-11-21

0.019275

-0.005837

0.003007

0.001167

1246 rows × 4 columns

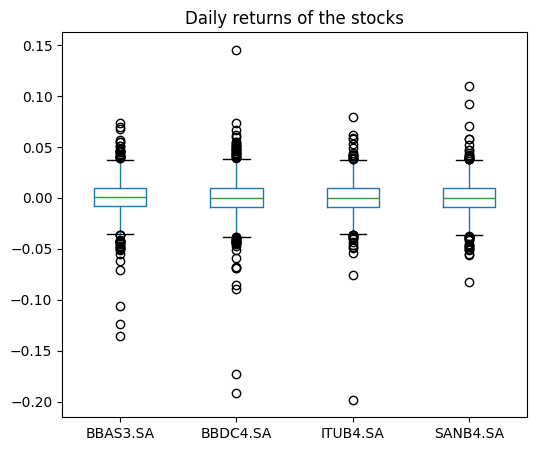

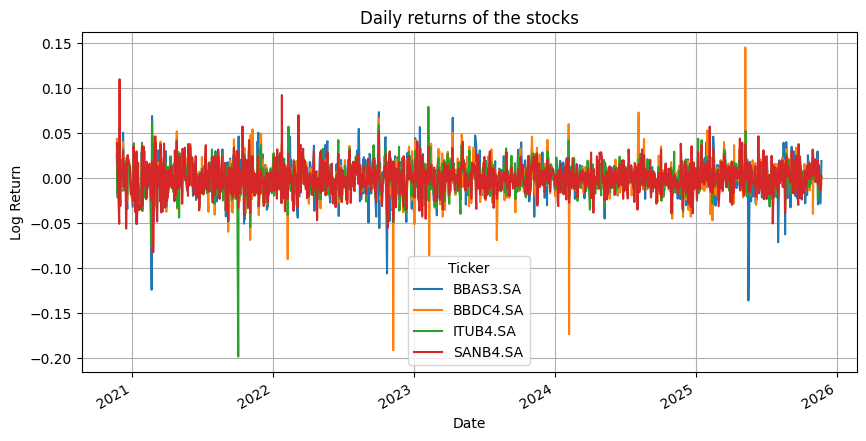

Then we can plot log returns and understand about conditional hererocedasticy and distribution

Código

import matplotlib.pyplot as plt# Boxplot of daily returnsdaily_returns.boxplot(figsize=(6, 5), grid=False)plt.title("Daily returns of the stocks");

Código

# Lineplot of daily returnsdaily_returns.plot(figsize=(10, 5))plt.title("Daily returns of the stocks")plt.xlabel("Date")plt.ylabel("Log Return")plt.grid(True)plt.show();

Código

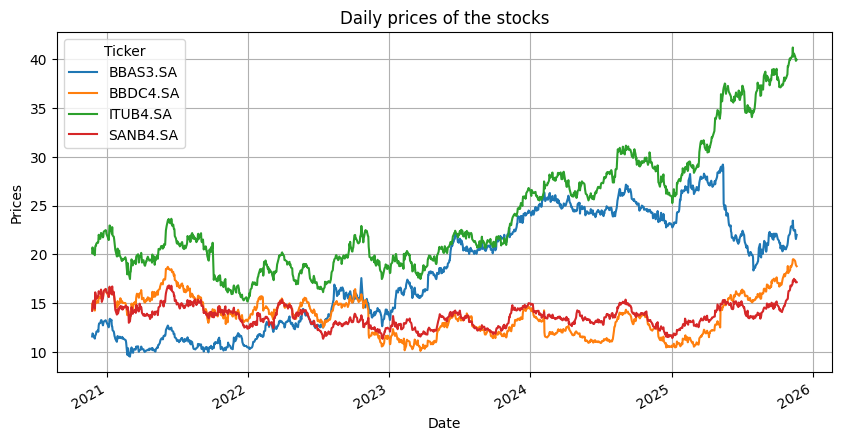

# Lineplot of pricesdata.plot(figsize=(10, 5))plt.title("Daily prices of the stocks")plt.xlabel("Date")plt.ylabel("Prices")plt.grid(True)plt.show();

Código

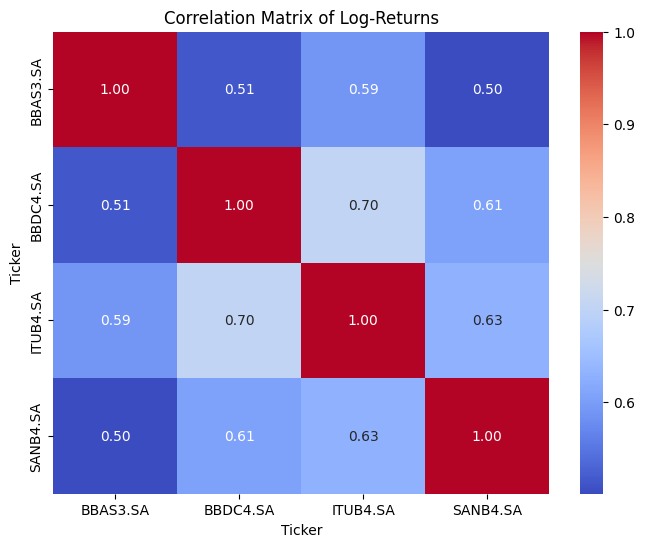

# matrix correlation of log-returnsimport seaborn as snscorrelation_matrix = daily_returns.corr()plt.figure(figsize=(8, 6))sns.heatmap(correlation_matrix, annot=True, cmap='coolwarm', fmt=".2f")plt.title('Correlation Matrix of Log-Returns')plt.show()

Código

# calculate historical volatility of log_returns (generated by AI)def historical_volatility(log_returns, annualizing_factor=252):"""Calculates the historical volatility of log returns. Args: log_returns: A pandas DataFrame of daily log returns. annualizing_factor: The number of trading days in a year (default is 252). Returns: A pandas Series of annualized historical volatility for each asset. """import numpy as npimport pandas as pd daily_volatility = log_returns.std() annualized_volatility = daily_volatility * np.sqrt(annualizing_factor)return annualized_volatility# Calculate historical volatility for the daily returnshistorical_vol = historical_volatility(daily_returns)print("\nHistorical Volatility:")historical_vol

Historical Volatility:

0

Ticker

BBAS3.SA

0.275599

BBDC4.SA

0.303753

ITUB4.SA

0.257582

SANB4.SA

0.269779

Now let’s calculate CAPM model for the assets. For this we need to pick up the market return

Código

#getting historic stock data from yfinancestocks_list = ['^BVSP']ibov = yf.download(stocks_list, period='5y')['Close']mkt_returns = log_returns(ibov)mkt_returns = mkt_returns.rename(columns={'^BVSP': 'mkt_return'})

Código

mkt_returns

Ticker

mkt_return

Date

2020-11-24

0.022168

2020-11-25

0.003156

2020-11-26

0.000853

2020-11-27

0.003152

2020-11-30

-0.015374

...

...

2025-11-14

0.003665

2025-11-17

-0.004741

2025-11-18

-0.003005

2025-11-19

-0.007316

2025-11-21

-0.003940

1246 rows × 1 columns

Código

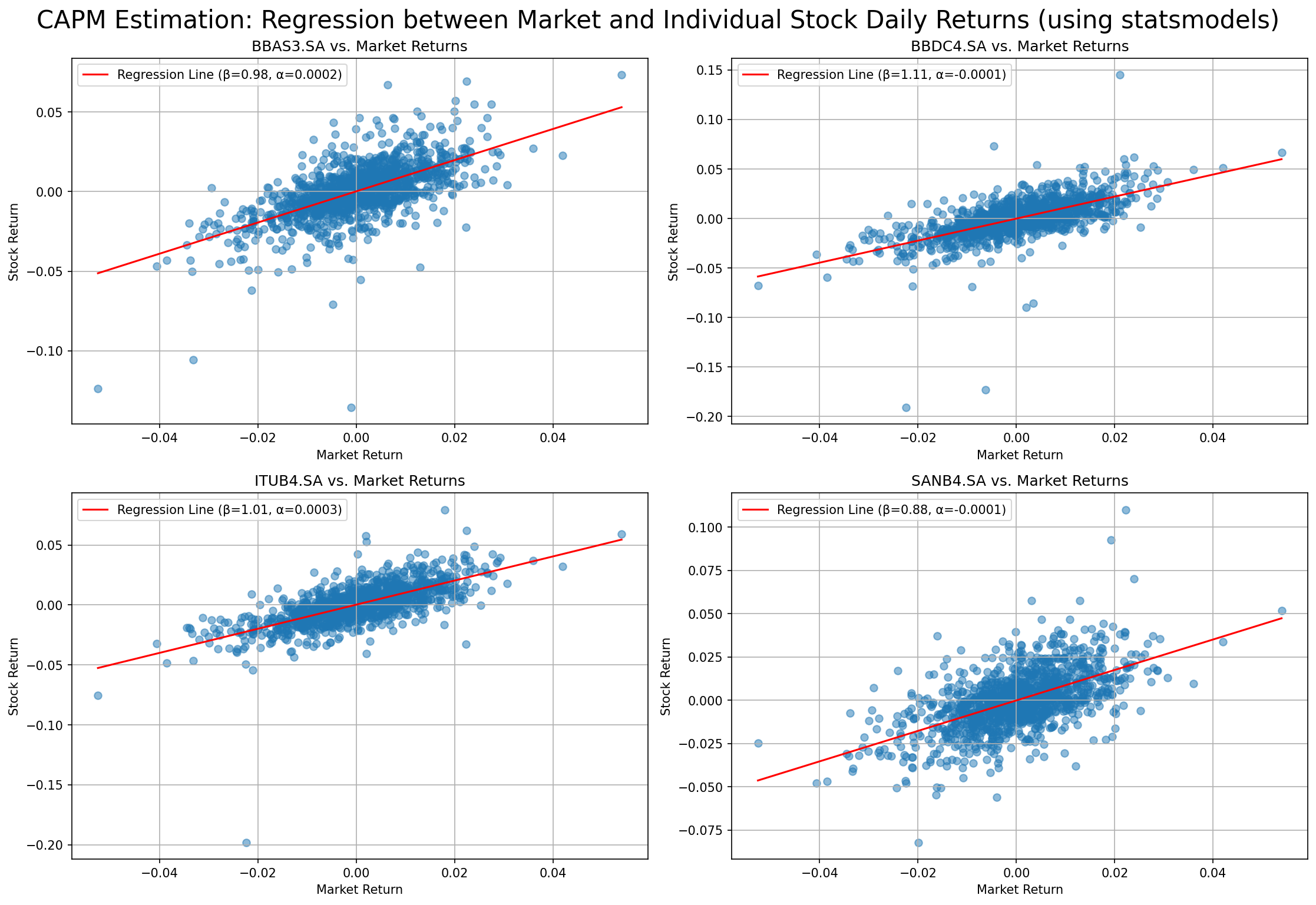

# prompt: capm model between log_returns and mkt_returnsimport statsmodels.api as smimport pandas as pdimport numpy as npimport matplotlib.pyplot as pltbeta_sm, alpha_sm =dict(), dict()# Loop through each stock to perform regressionfor stock in daily_returns.columns:# Define dependent and independent variables y = daily_returns[stock] X = mkt_returns['mkt_return']# Add a constant for the intercept (alpha) X = sm.add_constant(X)# Perform the regression model = sm.OLS(y, X).fit()# Extract beta and alpha beta_sm[stock] = model.params['mkt_return'] alpha_sm[stock] = model.params['const']# Print the regression results summaryprint(f"\nCAPM Regression Results for {stock}:")print(model.summary())print("\nBetas from statsmodels:")print(beta_sm)print("\nAlphas from statsmodels:")print(alpha_sm)

# Plotting the regressions using statsmodelsfig, axes = plt.subplots(2, 2, dpi=150, figsize=(15, 10))axes = axes.flatten()for stock in daily_returns.columns: idx = daily_returns.columns.get_loc(stock)if stock in beta_sm and stock in alpha_sm: X = mkt_returns['mkt_return'] y = daily_returns[stock]# Scatter plot axes[idx].scatter(X, y, alpha=0.5)# Add the regression line using the statsmodels results# Create a range of market return values for the line mkt_return_range = np.linspace(X.min(), X.max(), 100) regression_line = alpha_sm[stock] + beta_sm[stock] * mkt_return_range axes[idx].plot(mkt_return_range, regression_line, color='red', label=f'Regression Line (β={beta_sm[stock]:.2f}, α={alpha_sm[stock]:.4f})') axes[idx].set_title(f'{stock} vs. Market Returns') axes[idx].set_xlabel('Market Return') axes[idx].set_ylabel('Stock Return') axes[idx].legend() axes[idx].grid(True)else: axes[idx].set_title(f'{stock} vs. Market Returns - Data Missing') axes[idx].text(0.5, 0.5, 'Data Missing', horizontalalignment='center', verticalalignment='center', transform=axes[idx].transAxes)plt.tight_layout()plt.suptitle("CAPM Estimation: Regression between Market and Individual Stock Daily Returns (using statsmodels)", size=20, y=1.02)plt.show()

Código

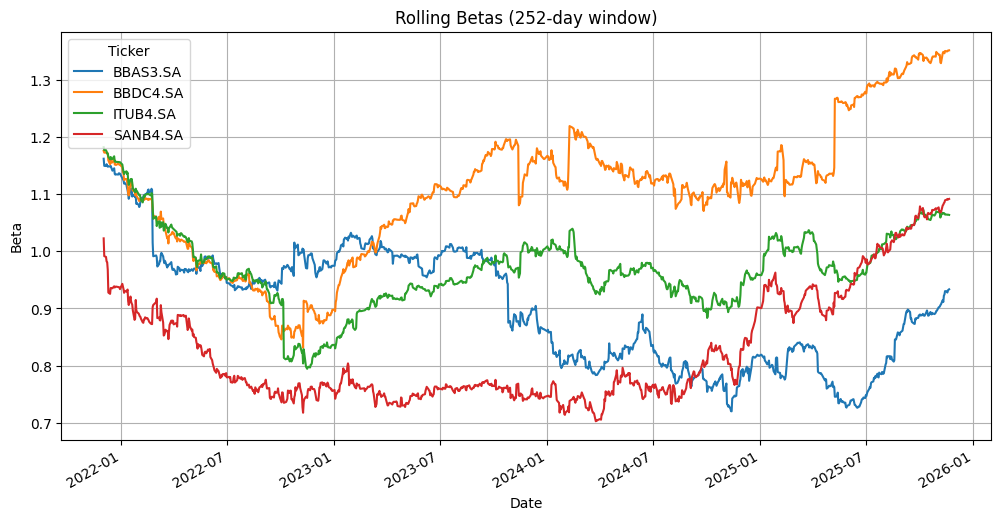

# prompt: rolling betas camp for daily_returns using statsmodels regressiondef rolling_betas_camp(daily_returns, mkt_returns, window):""" Calculates rolling betas for a list of stocks against the market using statsmodels OLS. Args: daily_returns (pd.DataFrame): DataFrame of daily log returns for the stocks. mkt_returns (pd.DataFrame): DataFrame of daily log returns for the market. window (int): The size of the rolling window. Returns: pd.DataFrame: DataFrame containing the rolling betas for each stock. """ rolling_betas = pd.DataFrame(index=daily_returns.index, columns=daily_returns.columns)for stock in daily_returns.columns:for i inrange(window, len(daily_returns)):# Define the rolling window window_returns = daily_returns[stock].iloc[i-window:i] window_mkt_returns = mkt_returns['mkt_return'].iloc[i-window:i]# Ensure there are enough data points in the windowiflen(window_returns) == window andlen(window_mkt_returns) == window:# Define dependent and independent variables y = window_returns X = window_mkt_returns# Add a constant for the intercept (alpha) X = sm.add_constant(X)# Perform the regressiontry: model = sm.OLS(y, X).fit()# Store the beta value rolling_betas.loc[daily_returns.index[i], stock] = model.params['mkt_return']exceptExceptionas e:# Handle cases where regression might fail (e.g., no variation in data)print(f"Regression failed for {stock} at index {daily_returns.index[i]}: {e}") rolling_betas.loc[daily_returns.index[i], stock] = np.nanreturn rolling_betas# Calculate rolling betas with a window of 252 trading days (approx 1 year)rolling_betas = rolling_betas_camp(daily_returns, mkt_returns, window=252)print("\nRolling Betas:")print(rolling_betas.tail())# Plot the rolling betasrolling_betas.plot(figsize=(12, 6))plt.title('Rolling Betas (252-day window)')plt.xlabel('Date')plt.ylabel('Beta')plt.grid(True)plt.show()

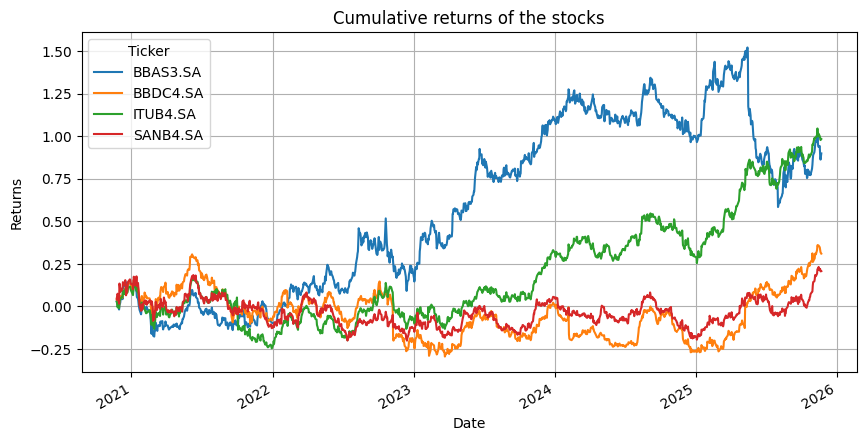

def calculate_cumulative_returns(returns):""" Calculates cumulative returns from a series of simple returns. Args: returns: A pandas Series or NumPy array of simple returns. Returns: A pandas Series or NumPy array of cumulative returns. """ cumulative_returns = (1+ daily_returns_level).cumprod() -1return cumulative_returns# Example usage:# Assuming you have a pandas Series of daily returns called 'daily_returns'# Example Datacumulative_returns = calculate_cumulative_returns(returns)print(cumulative_returns)

# Lineplot of daily returnscumulative_returns.plot(figsize=(10, 5))plt.title("Cumulative returns of the stocks")plt.xlabel("Date")plt.ylabel("Returns")plt.grid(True)plt.show();

Código

np.exp(mkt_returns)-1

Ticker

mkt_return

Date

2020-11-24

0.022416

2020-11-25

0.003161

2020-11-26

0.000854

2020-11-27

0.003157

2020-11-30

-0.015257

...

...

2025-11-14

0.003671

2025-11-17

-0.004729

2025-11-18

-0.003000

2025-11-19

-0.007290

2025-11-21

-0.003932

1246 rows × 1 columns

Código

mkt_returns

Ticker

mkt_return

Date

2020-11-24

0.022168

2020-11-25

0.003156

2020-11-26

0.000853

2020-11-27

0.003152

2020-11-30

-0.015374

...

...

2025-11-14

0.003665

2025-11-17

-0.004741

2025-11-18

-0.003005

2025-11-19

-0.007316

2025-11-21

-0.003940

1246 rows × 1 columns

Código

# Estimate the expected return of the market using the daily returnsER =dict()rf =0.1383#mkt_returns_level = np.exp(mkt_returns)-1rm = mkt_returns.mean()*252for k in daily_returns.columns:# Calculate return for every security using CAPM ER[k] = rf + beta_sm[k] * (rm-rf)print("Expected return based on CAPM model for {} is {}%".format(k, round(ER[k]*100, 2)))# Calculating historic returnsprint('Return based on historical data for {} is {}%'.format(k, round(daily_returns[k].mean() *100*252, 2)))

Expected return based on CAPM model for BBAS3.SA is Ticker

mkt_return 7.52

dtype: float64%

Return based on historical data for BBAS3.SA is 12.96%

Expected return based on CAPM model for BBDC4.SA is Ticker

mkt_return 6.67

dtype: float64%

Return based on historical data for BBDC4.SA is 5.45%

Expected return based on CAPM model for ITUB4.SA is Ticker

mkt_return 7.36

dtype: float64%

Return based on historical data for ITUB4.SA is 13.85%

Expected return based on CAPM model for SANB4.SA is Ticker

mkt_return 8.17

dtype: float64%

Return based on historical data for SANB4.SA is 3.8%

Código

rm

np.float64(0.07393662034276567)

Código

# prompt: calculate sharpe ratio of daily_returnsdef sharpe_ratio(returns, risk_free_rate=0):""" Calculates the Sharpe Ratio for a given series of returns. Args: returns (pd.Series or np.array): A series or array of returns. risk_free_rate (float): The risk-free rate of return (default is 0). Should be on the same frequency as the returns. Returns: float: The Sharpe Ratio. """ excess_returns = returns - risk_free_ratereturn excess_returns.mean() / excess_returns.std()# Calculate Sharpe Ratio for each stocksharpe_ratios = {}annualized_risk_free_rate = rf # Using the already defined annualized risk-free rate# Assuming the risk-free rate is given as an annual rate, we need to convert it# to the same frequency as the daily returns. For daily returns, we take the# daily equivalent risk-free rate.# daily_risk_free_rate = (1 + annualized_risk_free_rate)**(1/252) - 1# A simpler approximation is annual_rate / 252 for small rates.# Let's use the approximation for simplicity here, assuming rf is an annualized rate.daily_risk_free_rate = annualized_risk_free_rate /252for stock in daily_returns.columns: sharpe_ratios[stock] = sharpe_ratio(daily_returns[stock], daily_risk_free_rate)print("\nSharpe Ratios:")for stock, ratio in sharpe_ratios.items():print(f"{stock}: {ratio:.4f}")

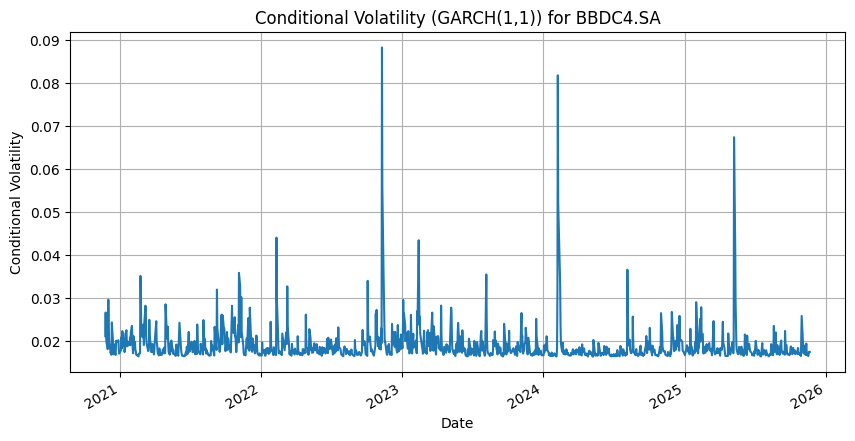

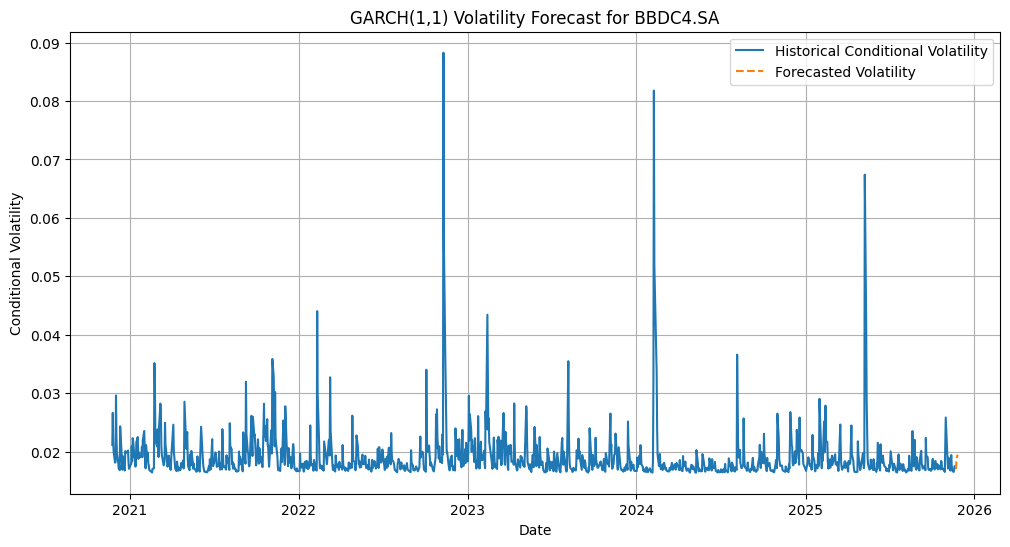

# prompt: Garch model volatility forecast for daily_returns!pip install archfrom arch import arch_model# Select one stock to model (e.g., BBDC4.SA)stock_to_model ='BBDC4.SA'returns_to_model = daily_returns[stock_to_model]# Fit a GARCH(1, 1) model# The `vol='GARCH'` specifies the GARCH process# The `p=1` and `q=1` specify the orders of the AR and MA terms for the variance equationam = arch_model(returns_to_model, vol='Garch', p=1, q=1)res = am.fit(update_freq=5)# Print the model summaryprint(res.summary())# Plot the conditional variance (volatility)fig = res.conditional_volatility.plot(figsize=(10, 5))plt.title(f'Conditional Volatility (GARCH(1,1)) for {stock_to_model}')plt.xlabel('Date')plt.ylabel('Conditional Volatility')plt.grid(True)plt.show()# Make a forecast of the conditional volatility# Forecast for the next 5 daysforecast_horizon =5forecasts = res.forecast(horizon=forecast_horizon)# The forecast object contains different types of forecasts.# We are interested in the volatility forecasts.# 'h.0' is the mean of the conditional variance forecast# 'h.1' are the quantiles (if calculated)# 'variance' is the forecast of the conditional variance itself# We need to take the square root of the variance forecast to get volatilityforecast_volatility = np.sqrt(forecasts.variance)# The forecast is given for the horizons starting from the last observation.# Get the index for the forecastlast_date = returns_to_model.index[-1]forecast_dates = pd.date_range(start=last_date, periods=forecast_horizon +1, freq='D')[1:] # +1 and [1:] to exclude the last historical dateprint(f'\nGARCH(1,1) Volatility Forecast for {stock_to_model} (next {forecast_horizon} days):')forecast_df = pd.DataFrame(forecast_volatility.iloc[-1].values, index=forecast_dates, columns=['Forecasted Volatility'])print(forecast_df)# Optional: Plot the historical conditional volatility and the forecastplt.figure(figsize=(12, 6))plt.plot(res.conditional_volatility.index, res.conditional_volatility, label='Historical Conditional Volatility')plt.plot(forecast_df.index, forecast_df['Forecasted Volatility'], label='Forecasted Volatility', linestyle='--')plt.title(f'GARCH(1,1) Volatility Forecast for {stock_to_model}')plt.xlabel('Date')plt.ylabel('Conditional Volatility')plt.legend()plt.grid(True)plt.show()

Requirement already satisfied: arch in /usr/local/lib/python3.12/dist-packages (8.0.0)

Requirement already satisfied: numpy<3,>=1.22.3 in /usr/local/lib/python3.12/dist-packages (from arch) (2.0.2)

Requirement already satisfied: pandas>=1.4.0 in /usr/local/lib/python3.12/dist-packages (from arch) (2.2.2)

Requirement already satisfied: scipy>=1.8 in /usr/local/lib/python3.12/dist-packages (from arch) (1.16.3)

Requirement already satisfied: statsmodels>=0.13.0 in /usr/local/lib/python3.12/dist-packages (from arch) (0.14.5)

Requirement already satisfied: packaging in /usr/local/lib/python3.12/dist-packages (from arch) (25.0)

Requirement already satisfied: python-dateutil>=2.8.2 in /usr/local/lib/python3.12/dist-packages (from pandas>=1.4.0->arch) (2.9.0.post0)

Requirement already satisfied: pytz>=2020.1 in /usr/local/lib/python3.12/dist-packages (from pandas>=1.4.0->arch) (2025.2)

Requirement already satisfied: tzdata>=2022.7 in /usr/local/lib/python3.12/dist-packages (from pandas>=1.4.0->arch) (2025.2)

Requirement already satisfied: patsy>=0.5.6 in /usr/local/lib/python3.12/dist-packages (from statsmodels>=0.13.0->arch) (1.0.2)

Requirement already satisfied: six>=1.5 in /usr/local/lib/python3.12/dist-packages (from python-dateutil>=2.8.2->pandas>=1.4.0->arch) (1.17.0)

Iteration: 5, Func. Count: 39, Neg. LLF: -3154.1819099755176

Iteration: 10, Func. Count: 67, Neg. LLF: -3188.1621902352554

Optimization terminated successfully (Exit mode 0)

Current function value: -3188.16219023508

Iterations: 10

Function evaluations: 67

Gradient evaluations: 10

Constant Mean - GARCH Model Results

==============================================================================

Dep. Variable: BBDC4.SA R-squared: 0.000

Mean Model: Constant Mean Adj. R-squared: 0.000

Vol Model: GARCH Log-Likelihood: 3188.16

Distribution: Normal AIC: -6368.32

Method: Maximum Likelihood BIC: -6347.81

No. Observations: 1246

Date: Mon, Nov 24 2025 Df Residuals: 1245

Time: 00:53:16 Df Model: 1

Mean Model

=============================================================================

coef std err t P>|t| 95.0% Conf. Int.

-----------------------------------------------------------------------------

mu 7.8979e-04 7.154e-04 1.104 0.270 [-6.125e-04,2.192e-03]

Volatility Model

============================================================================

coef std err t P>|t| 95.0% Conf. Int.

----------------------------------------------------------------------------

omega 1.7393e-04 5.969e-05 2.914 3.571e-03 [5.694e-05,2.909e-04]

alpha[1] 0.2035 0.125 1.627 0.104 [-4.170e-02, 0.449]

beta[1] 0.3491 0.175 1.994 4.618e-02 [5.922e-03, 0.692]

============================================================================

Covariance estimator: robust

# prompt: value at risk for daily_returns using volatility modelsdef calculate_value_at_risk(returns, confidence_level=0.95, model='historical', volatility_model=None):""" Calculates Value at Risk (VaR) for a series of returns. Args: returns (pd.Series): A series of returns. confidence_level (float): The confidence level for the VaR (e.g., 0.95 for 95%). model (str): The VaR model to use. Options: 'historical', 'parametric' (uses normal distribution), 'parametric_garch'. volatility_model: Fitted volatility model object (e.g., from `arch_model.fit()`) if model is 'parametric_garch'. Returns: float: The calculated VaR. """ alpha =1- confidence_levelif model =='historical':# Historical VaR: VaR is the quantile of historical returns VaR =-np.percentile(returns, alpha *100)elif model =='parametric':# Parametric VaR (Normal Distribution): VaR = - (mean + Z * std_dev)# Assuming mean is close to zero for daily returns, VaR approx -Z * std_dev# Z is the z-score corresponding to the confidence levelfrom scipy.stats import norm mean_return = returns.mean() std_dev_return = returns.std() z_score = norm.ppf(alpha) VaR =-(mean_return + z_score * std_dev_return)elif model =='parametric_garch'and volatility_model isnotNone:# Parametric VaR (using GARCH forecasted volatility)from scipy.stats import norm# Get the last conditional volatility from the GARCH model# This assumes you are calculating VaR for the next period based on the model forecasted_volatility = volatility_model.conditional_volatility.iloc[-1] mean_return = returns.mean() # You could potentially use forecasted mean if your model predicts it z_score = norm.ppf(alpha) VaR =-(mean_return + z_score * forecasted_volatility)else:raiseValueError("Invalid VaR model specified or missing volatility_model for 'parametric_garch'.")return VaR# --- Calculate VaR using different models ---# Select the stock for VaR calculationstock_for_var ='BBDC4.SA'returns_for_var = daily_returns[stock_for_var]# 1. Historical VaR (e.g., 95% confidence)var_historical_95 = calculate_value_at_risk(returns_for_var, confidence_level=0.95, model='historical')print(f"\nHistorical VaR (95%) for {stock_for_var}: {var_historical_95:.4f}")var_historical_99 = calculate_value_at_risk(returns_for_var, confidence_level=0.99, model='historical')print(f"Historical VaR (99%) for {stock_for_var}: {var_historical_99:.4f}")# 2. Parametric VaR (Normal Distribution)var_parametric_95 = calculate_value_at_risk(returns_for_var, confidence_level=0.95, model='parametric')print(f"\nParametric VaR (Normal, 95%) for {stock_for_var}: {var_parametric_95:.4f}")var_parametric_99 = calculate_value_at_risk(returns_for_var, confidence_level=0.99, model='parametric')print(f"Parametric VaR (Normal, 99%) for {stock_for_var}: {var_parametric_99:.4f}")# 3. Parametric VaR (using GARCH(1,1) volatility)# We need the fitted GARCH model object ('res' from the previous cell)if'res'inglobals(): # Check if the 'res' object exists var_parametric_garch_95 = calculate_value_at_risk(returns_for_var, confidence_level=0.95, model='parametric_garch', volatility_model=res)print(f"\nParametric VaR (GARCH(1,1) Volatility, 95%) for {stock_for_var}: {var_parametric_garch_95:.4f}") var_parametric_garch_99 = calculate_value_at_risk(returns_for_var, confidence_level=0.99, model='parametric_garch', volatility_model=res)print(f"Parametric VaR (GARCH(1,1) Volatility, 99%) for {stock_for_var}: {var_parametric_garch_99:.4f}")else:print("\nSkipping GARCH-based VaR calculation as the GARCH model ('res') is not fitted in this session.")

Historical VaR (95%) for BBDC4.SA: 0.0273

Historical VaR (99%) for BBDC4.SA: 0.0437

Parametric VaR (Normal, 95%) for BBDC4.SA: 0.0313

Parametric VaR (Normal, 99%) for BBDC4.SA: 0.0443

Parametric VaR (GARCH(1,1) Volatility, 95%) for BBDC4.SA: 0.0285

Parametric VaR (GARCH(1,1) Volatility, 99%) for BBDC4.SA: 0.0404